Calculates the excess kurtosis of the Student's t-Distribution.

Syntax

TDIST_XKURT(v)

- v

- is the degrees of freedom of the Student's t-Distribution (v > 4).

Remarks

- TDIST_XKURT is declared as deprecated. Please, use DIST_XKURT as TDIST_XKURT is listed here only for backward compatibility.

- The probability density function of the Student's t-Distribution is defined as:

$$f(t) = \frac{\Gamma(\frac{\nu+1}{2})} {\sqrt{\nu\pi}\,\Gamma(\frac{\nu}{2})} \left(1+\frac{t^2}{\nu} \right)^{-(\nu+1)/2}$$ Where:- $\Gamma (.)$ is the gamma function.

- $\nu$ is the degrees of freedom (i.e., shape parameter).

- The excess kurtosis of t-Distribution is defined as: $$\gamma_2= \frac{6}{\nu-4}$$ Where:

- $\nu$ is the degrees of freedom.

- IMPORTANT The Student's t-Distribution kurtosis is only defined for degrees of freedom values greater than 4.

- Special Cases:

- $ \nu\to 4^+$. $$\lim_{\nu\to 4^+}\gamma_2(\nu)=+\infty$$

- $ \nu\to \infty$. $$\lim_{\nu\to +\infty}\gamma_2(\nu)=0$$

Examples

Example 1:

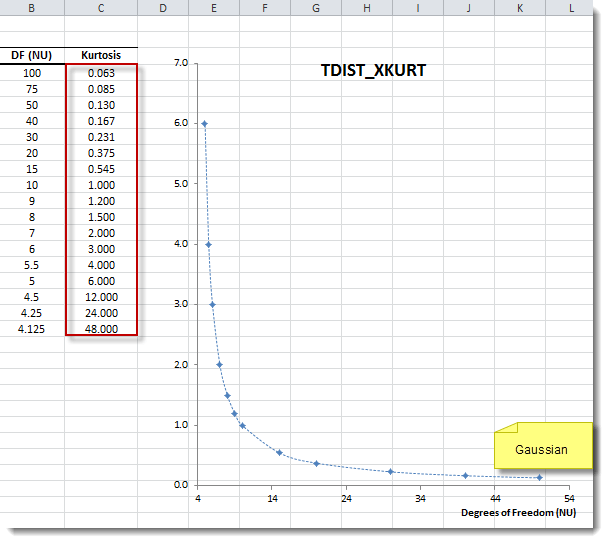

Student's t-Distribution X-Kurtosis Plot:

Example 2:

| Formula | Description (Result) |

|---|---|

| =TDIST_XKURT(5) | Excess kurtosis with 5 degrees of freedom (6.000). |

| =TDIST_XKURT(100) | Student t-dist approaches Normality as v >> 1 (0.063). |

| =TDIST_XKURT(4.002) | Excess kurtosis increases as v approaches 4 (3000.000). |

Files Examples

Related Links

- Financial Dictionary - Excess kurtosis.

- Wikipedia - Excess kurtosis.

- Wikipedia - Student's t-distribution.

References

- K.L. Lange, R.J.A. Little and J.M.G. Taylor. "Robust Statistical Modeling Using the t Distribution." Journal of the American Statistical Association 84, 881-896, 1989.

- Hurst, Simon, The Characteristic Function of the Student-t Distribution, Financial Mathematics Research Report No. FMRR006-95, Statistics Research Report No. SRR044-95.

Comments

Article is closed for comments.