To examine a given time series for signs of the ARCH Effect, we conduct a statistical test for evidence of white noise (Ljung-Box Test) between the squared input time series.

Similar to the regular white noise test, the hypothesis in question is:

$$H_{o}: \rho_{1}=\rho_{2}=...=\rho_{m}=0 $$

$$H_{1}: \exists \rho_{k}\neq 0$$

NumXL provides an intuitive interface to help Excel users conduct an ARCH effect using several lag orders. In this tutorial, we’ll demonstrate the steps to perform a thorough ARCH test using NumXL functions and wizards in Excel.

Process

- Select an empty cell to store the ARCH Effect tests results table.

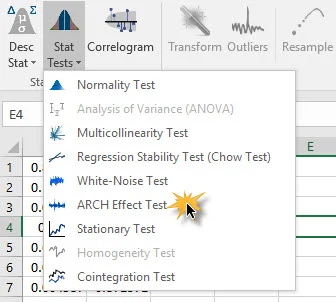

- Locate the Statistical Test (STAT TEST) icon in the toolbar (or menu in Excel 2003) and click on the down-arrow. When the drop-down menu appears, select “ARCH Effect Test”.

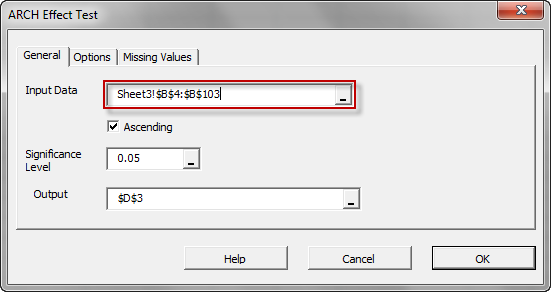

- The ARCH Effect Test dialog box appears.

- Select the cell range for the input data.

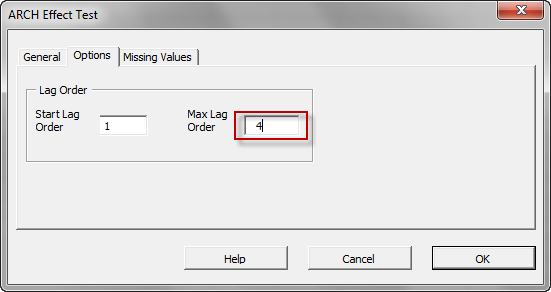

- Click the “Options” tab and pick a maximum lag order for this test.

- If your data include one or more intermediate observations with missing values, click the “Missing Values” tab.

- Click “OK”.

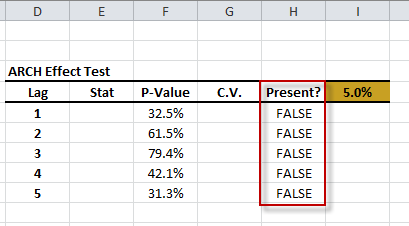

Output

The test wizard generates the ARCH Effect Test statistics for different lag scenarios.

Comments

Please sign in to leave a comment.