In modules five and six, we demonstrated a few steps to specify a model, calibrate the values of its parameters, and in module seven, we examined the standardized residuals – residuals diagnosis - to ensure the model proper fit with the input data.

In this module, we will take the final step and actually project a forecast: mean, standard error, and confidence interval.

In general, we are interested in forecasting the conditional mean and conditional standard deviation (aka volatility):

$$y_{T+k}=\mu_{T+k}+a_{T+k}$$ $$\mu_{T+k}=E_T [y_{T_k}]$$ $$a_{T+k}=\sigma_{T+k}\times\epsilon_{T+k}$$ $$\epsilon_{T+k} \sim \Phi(0,1)$$

Where

- $\mu_{T+k}$ is the conditional mean forecast at T+k

- $\sigma_{T+k}$ is the conditional volatility forecast at T+k

As a result; for a 95% confidence interval, the forecast is expressed as follows:

$$ \mu_{T+k}-1.96\times\sigma_{T+k}\leqslant y_{T+k}\leqslant \mu_{T+k}+1.96\times\sigma_{T+k}$$

For GARCH Models, the conditional mean is constant, so the forecast procedure is primarily focused on a volatility forecast.

$$\mu-1.96\times\sigma_{T+k}\leqslant y_{T+k}\leqslant \mu+1.96\times\sigma_{T+k}$$

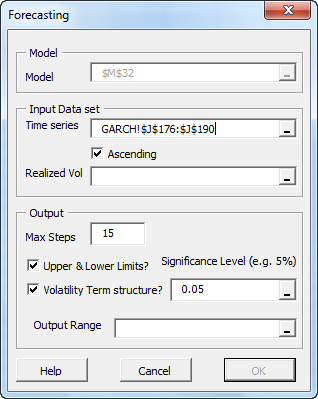

Using the NumXL forecast toolbar, you can generate the out-of-sample forecast values, standard errors and confidence intervals in a few steps.

- Select the first cell in the Model (i.e. M32)

- Locate and click on the Forecast icon in the NumXL toolbar

- The forecast wizard pops up on the screen.

- For input data, select the cell range of the latest (i.e. most recent) weekly log returns (~ July 2012).

- For the realized volatility, you may:

- Leave it blank, so that GARCH-fitted volatility is used, or

- Select a range of the latest weekly realized volatility (computed using a different approach)

- In the Output -> Max Steps field, select a 15-week forecast.

- In Output -> Volatility Term structure, leave it checked for now, as will discuss later on.

- In the Output Range, select an empty cell in your worksheet to print the forecast formulas.

- Click OK now.

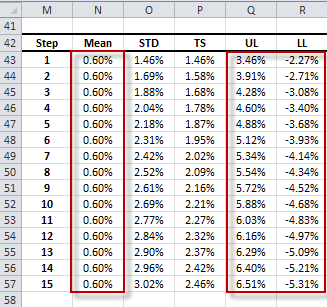

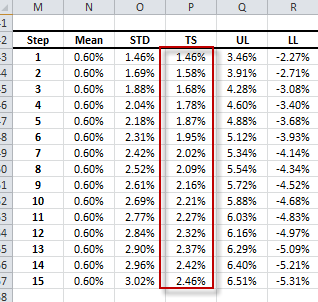

The forecast wizard prints the formulas for different cells in the forecast table (below):

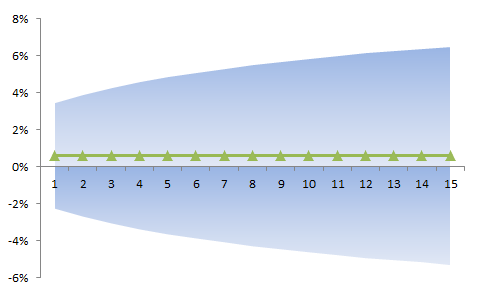

Furthermore, the forecast standard error (i.e. conditional volatility) is increasing with the forecast horizon (below).

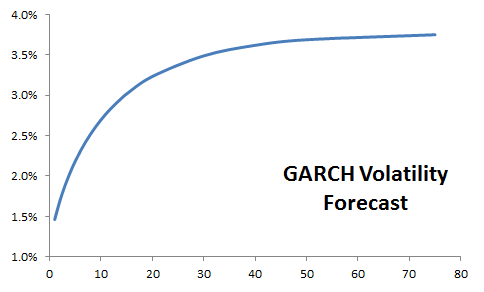

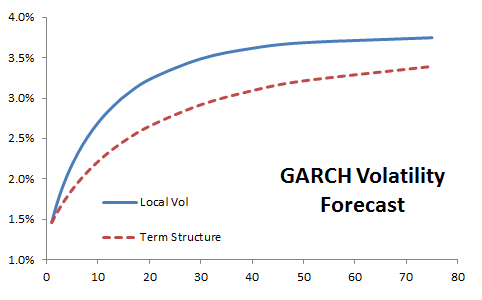

In the graph above, the volatility forecast climbs to its long-run value of (3.77%).

What are the long-run values?

For a stable time series model, the conditional mean and variance forecast converge to their long-run (historical or unconditional) values. The long-run values are implied (i.e. calculated) from the model’s parameter values.

Example: for GARCH(1,1), the long run conditional volatility (GARCH_VL) is expressed as follows:

$$\sigma_{T+\infty}=V_L= \frac{\alpha_o}{1-\sum_{i=1}^{\mathrm{max(p,q)}}(\alpha_i+\beta_i)}$$

Term Structure

In finance, we often wish to compute a multi-period volatility forecast (aka volatility term structure).

$$\sigma_{T\to T+k}^2 = \sigma_{T\to T+1}^2 + \sigma_{T+1\to T+2}^2 + \cdots + \sigma_{T+k-1\to T+k}^2$$ $$\sigma_{T\to T+k}^2 = \sigma_{T+1}^2 + \sigma_{T+2}^2 + \cdots + \sigma_{T+k}^2$$

Now we have a base-unit of $\sigma_{T\to T+k}^2$ expressed in terms of a k-period time unit. To facilitate comparison among different periods, we use a one-period time unit for all volatility calculations:

$$\sigma_{T\to T+k}^2 = \frac{\sigma_{T+1}^2 + \sigma_{T+2}^2 + \cdots + \sigma_{T+k}^2}{k}$$

Let’s plot the GARCH volatility term structure:

As for the multi-period log returns:

$$r_{T\to T+k}=r_{T\to T+1}+ r_{T+1\to T+2}+ \cdots + r_{T+k-1\to T+k}$$

And using the same time-unit base:

$$r_{T\to T+k}=\frac{r_{T\to T+1}+ r_{T+1\to T+2}+ \cdots + r_{T+k-1\to T+k}}{k}$$

For GARCH model, the conditional mean forecast is constant ($\mu$), so the multi-period returns (term structure) are also constant ($\mu$).

Application

Using the GARCH model earlier, what is the 3-month (12 weeks) volatility forecast per annum?

$$\sigma_{T\to T+12}^2 = \frac{\sigma_{T+1}^2 + \sigma_{T+2}^2 + \cdots + \sigma_{T+12}^2}{12}\times 52$$

This volatility value can be plugged into the Black-Scholes option pricing equation to generate a 3-month European S&P 500 index option.

Support Files

Comments

Article is closed for comments.