The ARIMA model is an extension of the ARMA model that applies to non-stationary time series (time series with one or more integrated unit-roots).

The ARIMA Model Wizard automates the model construction steps: guessing initial parameters, parameters validation, the goodness of fit testing, and residuals diagnosis.

Process

To use this functionality, select the corresponding icon on the toolbar (or the menu item):

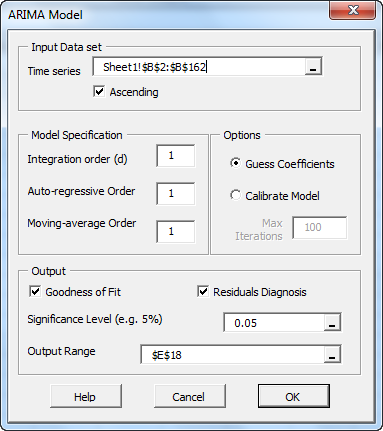

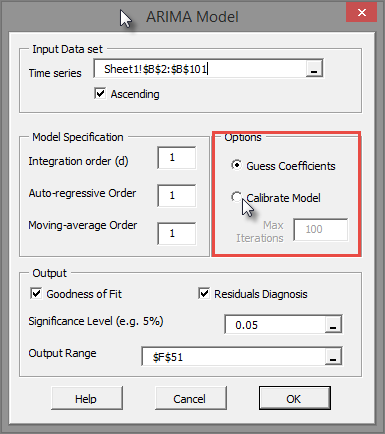

Rollover (select) the data sample on your worksheet and select the corresponding order of the autoregressive (AR) component model, integration order (d), and the order of the moving-average component model. Then select goodness of fit tests, residual diagnosis, and designate a location on your worksheet to print the model.

Note:

By default, the Model Wizard generates a quick guess of the values of the model’s parameters, but the user may choose to generate calibrated values for the model’s coefficients.

Output

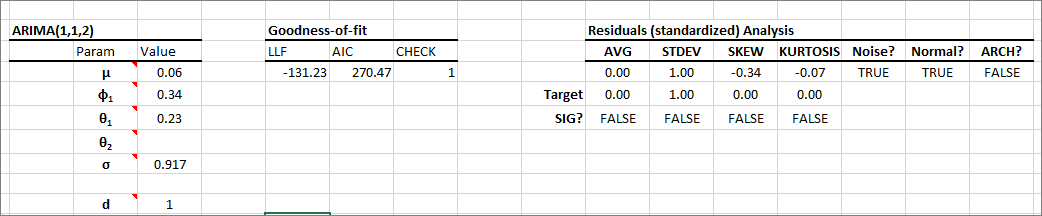

Upon completion, the ARMA modeling function outputs the selected model's parameters and selected tests/calculations in the designated location of your worksheet.

The ARIMA Wizard adds Excel-type of comments (red arrowheads) to the label cells to describe them.

Comments

Article is closed for comments.